Since we began managing Emerging Market equities 15 years ago, the asset class has transformed dramatically. What was once an opportunity set dominated by commodities, banks and low-cost manufacturing is now increasingly defined by AI infrastructure and internet platforms. This evolution is critically important because it places Emerging Markets at the centre of the largest investment cycle in a generation. In the following piece, we discuss how this occurred, the durability of the cycle, and the implications for portfolio construction.

From commodities to compute: the quiet revolution in Emerging Markets

There is a persistent mental model of Emerging Market equities that endures in the minds of many investors, despite having been substantially obsolete for well over a decade. Viewed through this outdated lens, EM is a play on commodities, demographics and low-cost export manufacturing. It is a world of iron ore miners, state-owned banks, oil majors, and consumer companies serving the newly aspirational middle classes of the Global South. Although elements of this paradigm remain true, it is woefully inadequate in capturing the reality of the asset class today.

A profound transformation has quietly reshaped Emerging Markets over the past fifteen years. Today – to a degree that would have seemed almost unimaginable in the 2000s – EM is primarily a technology play. The combined weight of IT and Communication Services now stands at 43.7% in the MSCI Emerging Markets index, versus 46.0% in the S&P 500.

This shift was driven by the compounding of several powerful forces: the secular decline in commodity prices after 2011, the explosive growth of Asian technology platforms, the listing and meteoric rise of China’s internet ecosystem, and the increasing concentration of the global semiconductor supply chain around a small number of Taiwanese and Korean champions.

Taiwan is the clearest example of this evolution. The prevailing narrative is that Emerging Markets have materially lagged the US over the past decade. Yet Taiwan has been a striking exception. In the ten years to April 2026, MSCI Taiwan generated a total return of 731% in US dollar terms, versus 314% for the S&P 500. On an annualised basis, this equates to returns of 23.6%, compared to 15.3% for the US market. As a result, Taiwan’s weight within the MSCI EM index has risen from 11.7% to 24.8%.

America’s buildout is Asia’s boom

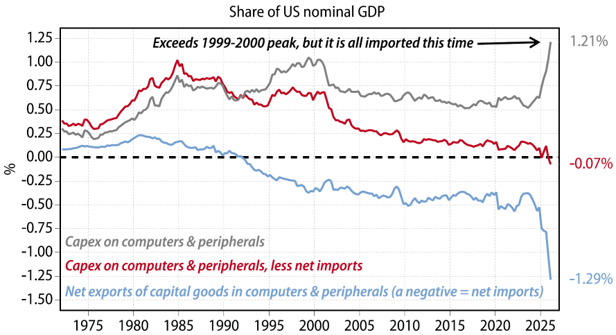

One of the defining features of the current macro environment is the vast capex cycle that the US is embarking on. AI infrastructure, reshoring, defence, electrification and energy security are collectively driving a surge in investment spending of extraordinary magnitude.

But the simple reality is that the US lacks the manufacturing capacity to supply itself. Consequently, Asia has become the primary transmission mechanism for this capex boom. Every dollar of hyperscaler capex generates up to a dollar of imports in semiconductors, equipment and components. Cash flow is therefore transferring from US hyperscalers to Asian technology manufacturers on an unprecedented scale.

US-driven investment requires Asian imports

Source: Gavekal Research/Macrobond

Taiwan and Korea are the main beneficiaries. Against a backdrop where hyperscaler capex is expected to approach $800bn in 2026, the combined free cash flow generation of just three semiconductor companies – Samsung, SK Hynix and TSMC – is forecast to reach $300bn this year.

Facing the same global opportunities and challenges as their US counterparts, governments and corporates across Asia are undertaking major investment programmes of their own. Spending on AI infrastructure, energy transition, industrial automation and defence is rising sharply across the region. A wide range of industrial indicators are already sitting at multi-year highs, and there is a growing possibility that Asia’s current capex and industrial cycle will be the strongest since the 2000s.

AI’s second wave: smarter models, stronger economics

In this context, we have maintained a positive view on the technology cycle and rapidly rising demand for compute, expressed through our longstanding overweight in tech hardware. However, given the vast amount of capital being committed to a nascent and still unpredictable technology, it is important to continually assess the sustainability of AI-related investment, appropriately discounting the obsolescence risk inherent to the sector.

Recent developments give us cause for continued optimism. The advent of agentic AI is an important evolution that strengthens our conviction to underwrite this investment cycle for longer. Earlier generations of AI models largely operated within a question-and-response ‘chatbot’ framework. By contrast, agentic models are iterative, collaborative and self-correcting. They are capable of running multiple protracted workflows that are far more compute-intensive than the single-task copilots they supersede. Consequently, token usage – effectively the volume of computation being performed – is rising exponentially. Goldman Sachs estimates that agentic AI could drive a 24-fold increase in current token consumption by 2030, with enterprise agents powering the next leg of growth and lifting token consumption 55X by 2040.

Whilst surging demand is important, token economics ultimately need to stack up if the AI value chain is to be sustainable. Here again there have been encouraging developments. Inference costs per token have declined as AI accelerator technology evolves from Nvidia GPUs towards increasingly sophisticated Application-Specific Integrated Circuit (ASIC) architectures such as Google TPUs and AWS Trainium. Annualised cost per token has fallen 60-70%, while token pricing has moved from persistent declines towards relative stability and, in some areas, increasing pricing power.

This apparent inflection in unit economics will be key to answering the defining question of this AI cycle: what is the return on investment in compute – for hyperscalers, frontier labs, and their end customers?

These dynamics resemble a modern manifestation of Jevons’ Paradox. Historically, technological efficiency gains have not reduced aggregate resource consumption, but instead increased it by expanding the range of economically viable use-cases. AI is still in its infancy, yet looks increasingly likely to follow the same pattern as its capabilities improve rapidly and its costs decline.

In just the past few days, AI has autonomously solved a prominent 80-year-old open problem central to the field of mathematics. This suggests that AI systems are becoming capable of sustaining long and difficult chains of reasoning, while connecting ideas across distant disciplines to generate novel solutions. It raises the tantalising prospect that these same abilities can accelerate progress in biology, physics, engineering, medicine and business. As frontier models evolve towards reasoning and logic, the practical applications of AI are becoming clearer, more monetisable and increasingly economically viable. All this points towards a longer technology cycle.

A barbell approach

This has important implications for portfolio construction. Hyperscaler capex is central to the investment case for much of the Asian technology hardware supply chain. It is well understood that these extraordinary levels of investment – expected to reach $1.1 trillion in 2027 – are causing substantial compression in free cash flow margins for US hyperscalers. We therefore believe it is increasingly important to differentiate between the quality and sustainability of different capex providers, acknowledging the circularity of some of the funding agreements between large players.

Not every dollar of investment spending is equal. Internally financed capex backed by robust free cash flow generation is materially more durable than investment dependent on debt or off-balance-sheet financing. In this context, we have greater conviction in supply chains aligned with hyperscalers possessing stronger balance sheets and more resilient business models.

For example, we prefer to invest in the supply chains of AWS rather than Oracle, where rising credit default swap spreads reflect growing balance sheet concerns. A company we view favourably in this context is Accton, whose positioning within Amazon’s Trainium ecosystem gives it significant exposure to AWS-related infrastructure demand. As hyperscalers accelerate their shift towards custom ASIC solutions, high-performance networking becomes ever more critical, given the growing complexity and scale of AI clusters. Accton’s strength in data centre switching and connectivity solutions places it at the centre of this transition.

Another company that we currently like is Hon Precision, a producer of integrated circuit test handlers and thermal control equipment used in back-end semiconductor testing, including for chips packaged on TSMC’s chip-on-wafer-on-substrate line. Its end customer base spans TSMC, Nvidia and leading outsourced semiconductor assembly and test companies such as ASE. Hon Precision is agnostic between competing chip architectures: whether AI compute scales through Nvidia GPUs or through custom ASIC solutions, all roads still lead through TSMC's advanced packaging and the testing steps that follow.

However, to bring the argument full circle, some of our strongest convictions actually sit outside technology in companies that represent the EM of yesteryear. These are ‘old economy’ businesses characterised by low obsolescence risk and structural scarcity value, particularly within the metals and mining, heavy industry and construction equipment sectors. As energy demand, electrification and industrial investment continue to accelerate globally, these sectors remain critically important enablers of the broader capex cycle.

Ultimately, we believe investors continue to underestimate both the scale and durability of the transformation underway within Emerging Markets. In our view, they represent one of the most compelling opportunity sets in global equities, and we have rarely been more optimistic about our portfolios.

Important information: This information is issued by TT International Asset Management Ltd (“TT”), authorised and regulated in the United Kingdom by the Financial Conduct Authority. This information is not intended for distribution to or use by any person or entity in any jurisdiction or country where such distribution or use would be contrary to local law or regulation. The circulation of this information is restricted to professional investors as defined in the legislation of the jurisdiction where this information is received. No representation is made as to the accuracy or completeness of any information contained herein, and the recipient accepts all risk in relying on this information for any purpose whatsoever. Without prejudice to the foregoing, any views expressed herein are the opinions of TT as of the date on which this information has been prepared and are subject to change at any time without notice. TT does not undertake to update this information. Any forward-looking statements herein are inherently subject to material business, economic and competitive risks and uncertainties, many of which are beyond TT’s control and are subject to change. The information herein does not constitute an offer of shares or units in any fund, and it is not an offer to, or solicitation of, any potential clients or investors for the provision by TT of investment management, advisory or any other comparable or related services. No statement in this information is or should be construed as investment, legal, or tax advice, nor is any statement an offer to sell, or a solicitation of an offer to buy, any security or other instrument, or an offer to arrange any transaction, or to enter into legal relations. This information expresses no views as to the suitability of the investments described herein to the individual circumstances of any recipient. Any person considering any investment should consult the offering documentation if and when is made available. Investments carries with it a high degree of risk. Past performance is not necessarily indicative of future results and investors may not retrieve their original investment.